The Mortgage Lock-In Effect Is Easing

For the past few years, the housing market has been defined by the so-called “lock-in effect,” with homeowners reluctant to give up historically low mortgage rates. While that dynamic hasn’t disappeared, new data shows it is beginning to loosen.

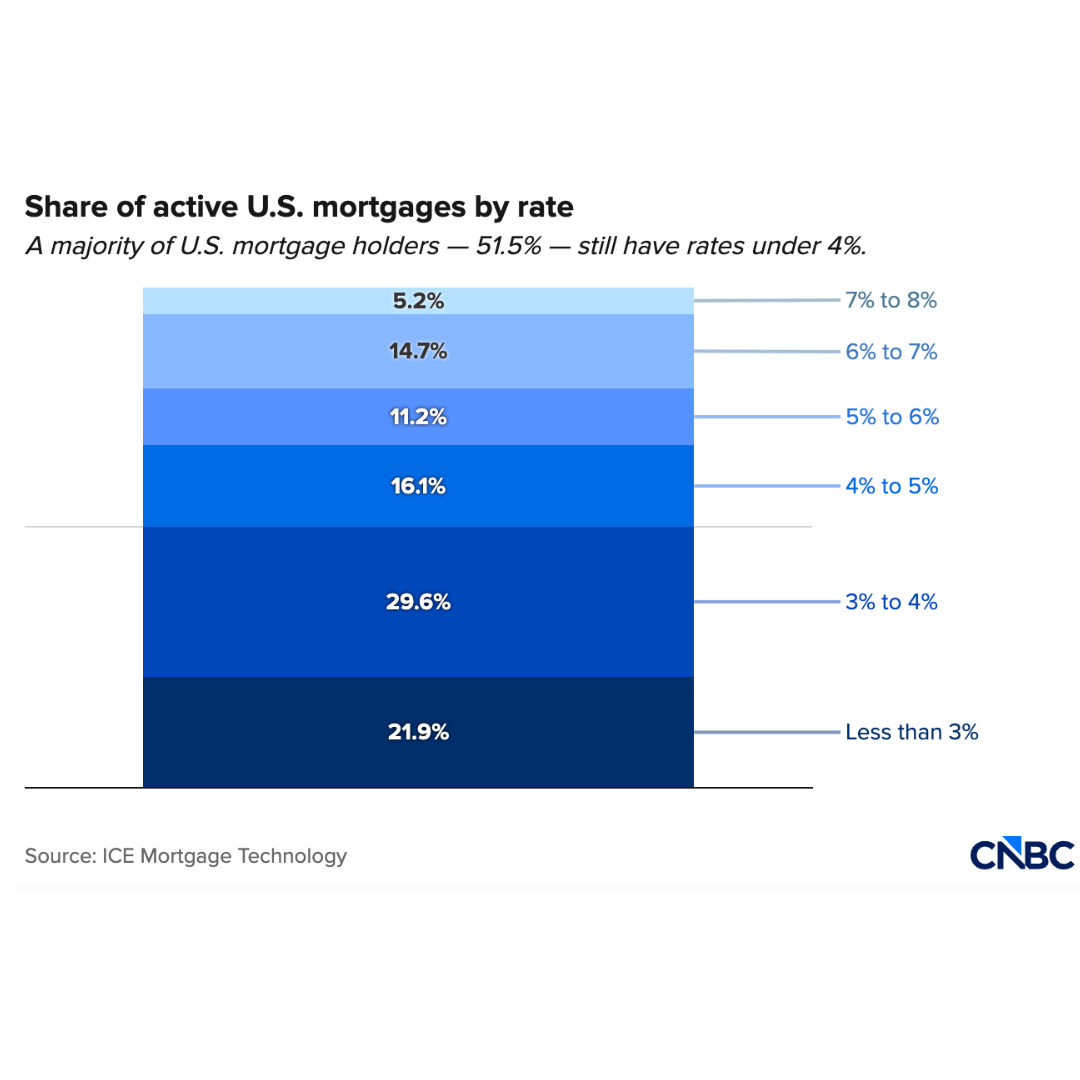

Today, more than half of U.S. mortgage holders still have rates under 4%, but the share of homeowners with rates above 5% has climbed sharply. In 2022, fewer than 10% of borrowers held mortgages above that level. Now, more than 30% do, and roughly 20% have rates over 6%, according to ICE Mortgage Technology. As more recent buyers entered the market at higher rates — and some homeowners tapped equity through refinancing — the pool of “rate-locked” owners has slowly shrunk.

That shift is already showing up in activity. Refinance applications are up roughly 120% year over year, and more homeowners are choosing to move despite higher rates, prioritizing lifestyle, family needs, or timing over holding onto an ultra-low loan. While modest rate declines may not dramatically change affordability for buyers, they are enough to encourage movement — and that movement is what gradually brings more inventory and momentum back to the market.